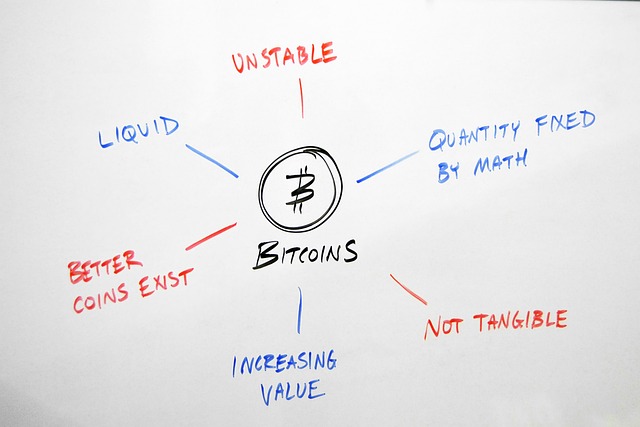

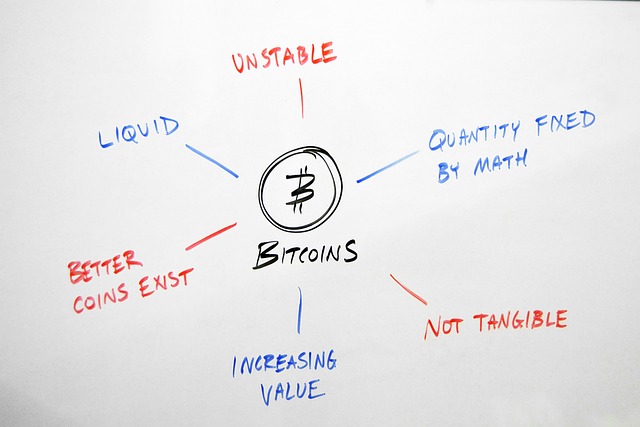

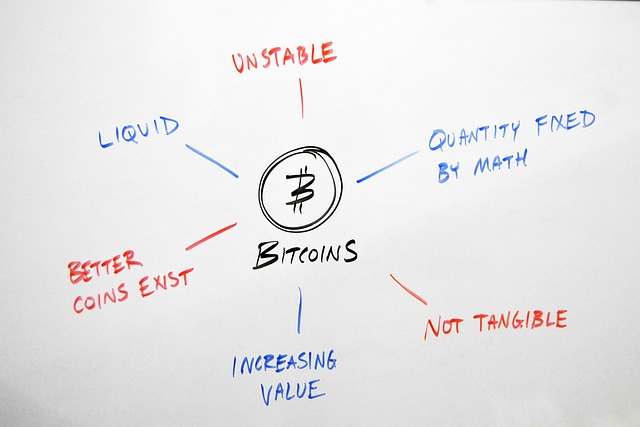

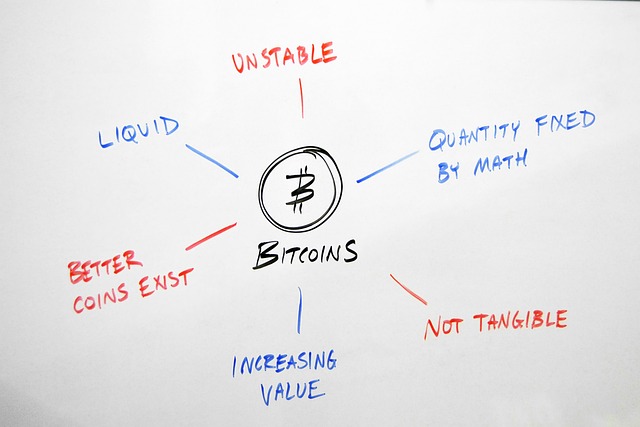

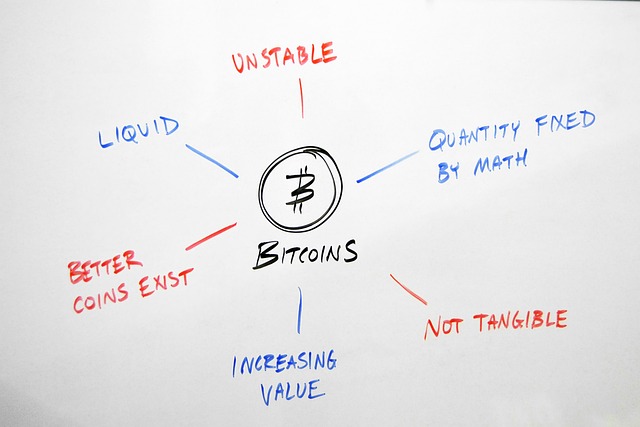

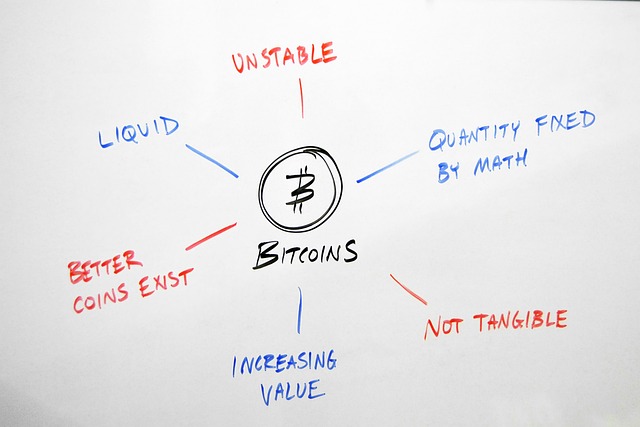

Online checks offer instant access, convenience, and real-time updates but face security concerns and digital divides. Traditional checks provide tangible security and immediate transaction visibility but have slow processing times, environmental impact, and paper waste. Digital transactions gain traction due to cost-effectiveness, despite challenges like heightened security risks and internet reliance. Balancing fraud prevention measures is crucial for online check security. User experience preferences drive consumer choices between digital innovations and traditional methods, with generational gaps persisting.

In today’s digital age, the evolution of payment methods has led to a debate between traditional checks and their online counterparts. This article delves into the contrasting worlds of online and traditional checks, examining their unique advantages and drawbacks. From instant access and convenience to tangible security and cost-effectiveness, we explore the pros and cons of each, ultimately shedding light on how they shape our financial interactions.

- Online Checks: Instant Access and Convenience

- Traditional Checks: Tangible Security Measures

- Cost Analysis: Digital vs Physical Transactions

- Speed and Efficiency: Digital Overhead Reductions

- Fraud Prevention Strategies: Digital Innovations

- User Experience: Preferences and Adoption Rates

Online Checks: Instant Access and Convenience

Online checks offer instant access and unparalleled convenience, making them a preferred option for many in today’s digital era. With just a few clicks, individuals can send payments to anyone, anywhere, at any time—a stark contrast to the traditional check system, which involves physical writing, printing, and mailing. This accessibility is particularly beneficial for businesses and individuals who need to manage multiple transactions frequently. Moreover, online checks provide real-time transaction updates, allowing users to track their finances with ease.

However, there are certain pros and cons to consider. While speed and convenience are undeniable advantages, security concerns often arise with digital transactions. Online checks require robust cybersecurity measures to protect sensitive financial data from cybercriminals. Additionally, not all individuals have equal access to technology, creating a potential digital divide that traditional checks can bypass.

Traditional Checks: Tangible Security Measures

Traditional checks offer a tangible security measure that many still find reassuring. The physical act of writing, signing, and mailing a check provides a sense of control and verification. This method allows for immediate visibility of transaction details, as recipients can see the precise amount, date, and payer information. It’s a straightforward process that doesn’t rely on technology, ensuring accessibility for those without consistent internet access or digital literacy.

However, traditional checks have their drawbacks when compared to online alternatives. The process is often slower, with delays in clearing and processing, leading to potential issues with timely payment confirmation. Additionally, there’s a higher risk of loss or theft during mailing, as well as the environmental impact of paper waste. These factors highlight the growing preference for digital solutions that offer speed, efficiency, and reduced environmental concerns in financial transactions.

Cost Analysis: Digital vs Physical Transactions

When comparing the cost analysis of digital transactions versus physical checks, it’s evident that online payments offer several advantages in terms of efficiency and pricing. One of the primary pros of online transactions is the significant reduction in processing fees. Traditional check processing involves various intermediaries, leading to higher costs for businesses. These overheads include bank charges, clearing house fees, and the labor involved in manual data entry. In contrast, digital payments often have lower transaction fees or even offer free processing, making them more cost-effective for both businesses and consumers.

However, there are also cons associated with online transactions. Security concerns and the need for robust cybersecurity measures can increase operational costs for businesses accepting digital payments. Additionally, certain industries may still rely on physical checks due to regulatory requirements or customer preferences. Despite these considerations, the overall trend suggests that as technology advances, the cost advantages of digital transactions will continue to drive their adoption, potentially reshaping the financial landscape.

Speed and Efficiency: Digital Overhead Reductions

The transition from traditional checks to digital transactions offers a multitude of benefits, particularly in terms of speed and efficiency. Online checks eliminate the need for manual processing, reducing overhead costs and processing times significantly. With just a few clicks, funds can be transferred directly from one account to another, making payments instant and convenient. This digital approach minimizes the reliance on physical paper, streamlining operations and allowing businesses to process a higher volume of transactions in less time.

However, while online checks present numerous advantages, they also come with certain drawbacks. Security concerns top the list, as sensitive financial data transmitted digitally requires robust encryption to protect against cyber threats. Additionally, internet connectivity becomes a critical factor; disruptions or failures can halt the entire process, causing delays and potential inconvenience for both senders and recipients. Despite these challenges, the pros of digital checks continue to drive their increasing adoption, reflecting a significant evolution in how financial transactions are conducted in today’s digital era.

Fraud Prevention Strategies: Digital Innovations

The digital revolution has brought about significant changes in the way financial transactions are conducted, with online checks becoming an increasingly popular alternative to traditional paper checks. In terms of fraud prevention, digital innovations offer both pros and cons when comparing online versus traditional checks.

On the positive side, online check processing leverages advanced technologies like encryption and secure databases to safeguard sensitive data. Digital signatures, biometric authentication, and real-time transaction monitoring are game-changers in mitigating fraudulent activities. These strategies provide multiple layers of security, ensuring that both the payer and payee remain protected. However, concerns about cybersecurity threats, such as phishing scams and identity theft, cannot be overlooked. As digital platforms become more accessible, so do opportunities for cybercriminals to exploit vulnerabilities, making it crucial to implement robust fraud prevention measures and keep up with evolving security protocols.

User Experience: Preferences and Adoption Rates

The user experience associated with both traditional checks and their digital counterparts plays a significant role in shaping consumer preferences and adoption rates. Online banking, including digital checks, offers several advantages from a user perspective. Customers can easily access their accounts from anywhere at any time, eliminating the need to visit a physical bank branch. This convenience is particularly appealing to younger generations who are more tech-savvy and value digital accessibility. Moreover, online check creation and submission processes often involve straightforward interfaces, allowing users to manage their finances with minimal effort.

In contrast, traditional checks provide a tangible and familiar experience for those accustomed to paper-based banking. They offer a sense of security and control that some consumers prefer, especially when it comes to sensitive financial transactions. While the adoption of digital checks is on the rise, particularly among millennials and Gen Z, there are still a significant number of individuals who rely on traditional methods due to trust issues with technology, concerns over data privacy, or simply personal preference. This divide in user preferences highlights the ongoing competition between the pros and cons of online banking and traditional checks.